You are here: Negligence and Error in Surveys and Valuations: The Margin for Error Revisited

As is always the case in a downturn, lenders and borrowers tend to turn to the one party in the process who holds professional indemnity insurance to try and recoup some of their losses; the valuer. The period of instability following the onset of the Global Financial Crisis (GFC) has been no exception.

Although few negligence cases actually reach court, there have been a number of cases where some key aspects of the negligence and error issues have been developed and refined recently. These have included developments in the 'margin for error' question – what level of valuation is deemed to be negligent, a question that the courts and valuers have been arguing about for many years, as well as rulings on contributory negligence, the extent of loss and on valuing in thin and unstable markets.

This paper reviews where we currently stand on these questions but also delves deeper, into some potential causes of error that you may not be aware of. As well as having nearly 25 years experience as a surveyor, Dr Havard's PhD was on valuation variance and error, and he revisits his findings a decade on.

Introduction: Current Position with Valuation Negligence Cases

It is no surprise that negligence actions against valuers and downturns are strongly connected, and that most of the actions that end up in court (which tend to be a small fraction of the total) tend to be in the years after the downturn, when the market has started to recover.

The reasons for this pattern are often obvious but some might be a little more obscure –

- Firstly lenders are seeking to recoup losses made on the loan. The one party in the equation with PI cover is the valuer – QED

- The action tends to be delayed because the extent of the loss the lender is claiming is not established at the normal trigger point; the default on the loan. It usually has to be proved by the disposal of the property interest against which the loan has been made. Particularly since 2008 this has led to delays [Note: Normally actions have to be started within 6 years of the event, hence it might be thought that valuations done in the period leading up to the recession (2006-2008) would be either out of time or about to fall out of this period. In fact actions are allowed within 3 years of discovering the loss, hence valuations in this period are not clear, indeed one of the cases I will be looking at below came to court in 2011 but related to a valuation in 2001.]

- To expand on this point, negligence cases hinge on three interconnected factors:

Negligence ---> Causation ---> Loss

Firstly, can the valuer be proved to have been negligent? If yes, then did the negligent valuation cause the parties to act differently than they would have if they had received a competent valuation? If that can be shown to have acted in this way what, then, is the loss that suffered as a result? To have a judgement against the valuer all three have to be established. The loss area tends to delay cases coming to courts.

Why do these negligence cases come about? Remember that it is generally taken that a valuer will be deemed to be negligent if the standard of the valuation they produce falls short of that of a reasonably competent valuer. How is this assessed? Distilling down the facts from case law puts valuation negligence into two broad categories:

- Mistake, carelessness or incompetence – This is where a valuer has really messed up, miss-measured, missed something important, calculated something wrong. These cases are pretty open and shut and actually rarely make it to court unless the court is asked to judge on the extent of damages. The recent case of Capita Alternative Fund Services (Guernsey) Limited and Matrix Securities Limited V Drivers Jonas [2011] (the case where the valuation dates back to 2001) is a rare exception. The subject property was a Factory Outlet Centre (FOC) in an Enterprise Zone, where Drivers Jonas failed the competence to act test, lacking experience in valuing FOCs and also about EZ tax vehicles, and, as a result, missed or failed to investigate key components. Even here, however, the key measure of negligence was whether the valuation fell within an acceptable margin (DJ valued at £48.1m – a competent valuation was assessed as being between £31.9m and £36.7m). Note that the damages were assessed at the difference between what the companies paid for the property and what they would have paid for it based upon an accurate valuation. In this case this was an eye-watering £18m.

- The valuation produced is outside an accepted ‘margin for error’ – There is often no technical mistake here, just that valuation produced, which is, after all, an opinion and not a definite concrete sum, is outside the boundaries of what a competent valuer would be expected to produce.

It is this latter case which tends to make it to court and the one that we will be concentrating on as it is often the most contentious. However both types of error tend to be most prevalent (or at least most auctioned) after a recession and refer to a period at or before the peak in the market.

Why? Well some of the reasons are down to nature of the market and the valuer’s work environment -

- The period leading up to the top of a market tends to be one of increasing volatility and uncertainty. Signals from the market are often mixed. It is hard to spot the turning points in the market

- Often at these times the workload of the valuer becomes more intense. Markets often show classic signs of ‘overheating’ – transactions are rushed often because the participants, buyers and lenders, can see a period of uncertainty or change is coming and rush to complete deals. The pressure on the valuers at this time is intense and – in my opinion – this is the time when they are at most risk at either making a mistake or being rushed into an ill-considered opinion.

- These actions will generally only take place when there has been negative price inflation – that’s a convoluted way of saying where prices/values have fallen. The reason why I used it is that positive price appreciation – capital appreciation/price rises – are the valuers’ friend. It is probable that there are as many valuations which might be otherwise construed as being negligent under the ‘margin of error’ concept whilst values are rising that never get auctioned because the valuation errors are hidden by the subsequent rise in prices.

There are other, contributory factors as well (and these are often used by valuers in defence of actions) –

- In this period, borrowers show clear tendencies to be either risk seeking or risk blind. ‘Must buy or miss out’ mindset.

- Similarly, lenders tend to be more reckless in their lending behaviour. Brokers within financial organisation only make money by broking deals; if a credit risk exercise stops a deal going ahead then no fee is earned. Credit risk assessment in financial organisations is seen in a negative light, either as a tick box exercise to provide a paper trial for compliance or as a barrier to overcome not in its true, intended role.

The combination of these two factors is to make lending more reckless in this overheating period in the market and it more likely that more financial arrangements that will be created that are more likely to fail – and note that the valuer knows little or nothing of these characteristics yet it is the valuer upon which the burden of their failures fall.

A further contributory factor in the current incidence of negligence is the status of the valuer – how much the role is ‘valued’ if you like – which has been eroded over the last 20 years, something for which I believe the RICS is culpable. The function of the valuer has been reduced from a true independent expert recording their opinion of value to, too often, being a tick box driven, deal making exercise. Fees have been driven down, the panel approach has seen valuers treated as being all the same, as interchangeable as light bulbs rather than selected as local experts, left to become the fall guys or girls if the underlying deal goes wrong.

I know expressing this opinion really doesn’t help valuers with this issue – but it’s still a sad state of affairs and simply wrong and the RICS is failing its members in allowing this to happen.

Cannot do much about mistake or omission, though these are more likely to happen where the valuer is under pressure in an unstable market, however we do need to look in more detail at the other main area of proof of negligence; margin for error as well as defences against claims for contributory negligence.

The Margin for Error – So where do valuers currently stand?

The margin for error is a long established (and probably ill-used) concept that has been developed over time in case law. It has sometimes been suggested as being +/- 10% or sometimes 10-20% but in fact is considerably more refined than that. In the early days of the margin for error (and certainly when I was doing my PhD work in the late 1990s) it was often used by the courts in isolation, with little apparent willingness to investigate or understand the circumstances of the valuation, being used as a quite blunt instrument as a measure of negligence. Recent case law has suggested that it is still being used but in a much more sophisticated way as part of the process of determining negligence.

A starting point to assess where valuers stand in regard to the margin of error are the comments of J Coulson in K/S Lincoln v CBRE Hotels (2010):

- For ‘standard’ residential property, the margin of error could be as low as +/- 5%

- For a valuation of a one-off property, the margin of error will usually be +/- 10%

- If there are exceptional features of the property, the margin of error could be +/- 15% or even higher in an appropriate case.

This was referred to by J Coulson himself in two important recent cases, Webb Resolutions and Blemain Finance, both of which involved E.Surv Ltd, which allows us to explore what the courts have said and also what might be inferred/suggested about the application of the principles.

In the former case there were two properties with two lenders involved, Mr Ali who purchased a flat in Birmingham valued at £227,995 (‘correct’ value £204,658) and Mr Bradley, remortgaging a 4 bedroom house in Whitstable valued at £295,000 (£260,000). As both properties were taken to be ‘standard’ and there were lots of comparables the correct margin was taken to be +/- 5% and the valuations were negligent.

In the latter case, the property was a 5 bedroom house in a private road in Putney. This was valued by E.Surv at £3.4m though the true market value was £2.8 m at the time of the valuation. This 21% variation was held to be negligent however J Coulson did hold that the correct measure for this property was 10% as it was ‘distinctive’.

However it should be noted that J Coulson did not look at the margin for error in isolation but also examined the methodology used by the E.Surv valuers (and this is something we will return to below). They failed to inspect the properties and they used asking prices rather than sale prices of the comparables, and there is no doubt that this made the judgement against them easier.

To show the variation in the interpretation of the margin for error but also showing how the courts will look at wider factors, J Keyser in Paratus AMC (GMAC) v Countrywide Surveyors (2011), although referring to Lincoln v CBRE, preferred to rely on the range of acceptable valuations produced by the respective parties’ expert witnesses which produced an 8% range – the valuation was actually on the edge of the 8% margin but was found to be not negligent. Judge Keyser commented (my commentary in square brackets):

- The 10% margin produced a relatively wide range of monetary figures [This implies that he felt that 10% was far too wide]

- The comparable evidence for the property lacked consistency and clarity, even though that the subject was a flat in a development of purpose-built flats completed in stages in the preceding year [This is helpful; it shows that some judges are looking at market conditions and how that otherwise ‘standard’ properties in the 5% bracket can be made more difficult by the evidence];

- That the market was buoyant, even volatile at the time (July 2004) [note the time lag as discussed earlier] and the market was still rising after a very substantial rise in the preceding years ;

- The general buoyancy of the market was heightened, in this particular case, in the Summer of 2004 as the glut of properties that had been available in 2003 was over and the opportunity to buy one was more limited [this underlines the point I made about market participants feeling like they are ‘missing out’ and perhaps tending towards financially irrational decisions].

All of the above presented the valuer with difficulties that would not normally exist in the valuation of residential flats, hence the widening of the Margin of Error to 8%.

General Comments on Margin for Error

- ‘Normal’ properties with lots of evidence margin can be as low as +/- 5%

- Market conditions can raise these margins

It is reassuring that the courts, whilst not always consistent in the actual margins allowed, are at least looking carefully at the circumstances in which the valuer is working.

From the commercial side of things, we can also draw a number of conclusions.

Where does this leave commercial properties? Well as it is generally accepted that commercial property is less homogenic than residential and, logically, will have less direct comparables in the vast majority of situations, this implies that mainstream commercial property will be more like the ‘one off’ residential and that the margin accepted will normally be at least 10% and often be higher. This is supported by the bulk of case law. It also suggests that the margin accepted in what is generally accepted to be the most volatile of markets – development land and development valuations, will be the ones that fall in the +/- 15% margin. This also seems to apply to the more specialised types of commercial property, especially where the market is thin.

We will return to the question of ‘The margin for error’ at the end of the paper.

Contributory Factors that can mitigate claim

Strictly, this is outside of the scope of this paper, but, for completeness, it is worth reviewing what counter claims that can be made to mitigate the claim of loss against a valuer. In the E.Surv cases, E.Surv alleged that the respective lenders in each case had negligently failed to look after their own interests and that this had caused (to some degree at least) the losses that were the subject of the claims. These allegations included: (i) high (and therefore "risky") loan-to-value ratios (LTV); (ii) self-certification of income; (iii) high levels of borrower indebtedness; (iv) the existence of warning signs (eg existing defaults/reliance on credit cards); (v) the correctness of affordability calculations (for example secure debt to income as opposed to total debt to income); and (vi) insufficient attention being given to errors or omissions on the applicant borrower's mortgage application forms.

When considering the appropriate standard against which GMAC[Webb resolutions]/Blemain's lending practices should be measured, Coulson J said that he should be "wary" of concluding that banking practices that were logical or commonplace to the practice or policy of a particular category of lender at the time were in fact illogical or irrational and therefore negligent. He stressed that allegations of contributory negligence on these bases must always be judged in light of the facts and against the context of the lending market at that particular time, in this case during the over-heated market around 2007 when lending policies were "over-generous". In only one of the 3 valuations in GMAC/Blemain were there found to be contributory negligence – in one of the Webb Resolutions the lending was at 95% to a customer who had very significant debts. Even here the damages were only reduced by 50%.

This underlines the fact that valuers cannot rely on whether the loan is sound or that the lender has acted prudently. There may be some comfort here but lender negligence has to be particularly bad!

The Margin For Error – A Wider Overview

Most CPD papers on the margin for error, particularly if delivered by someone with a legal background, would probably leave things there – they have looked at the case law and established where we have got to and then send people off on their way. As a valuer who has always been interested in the subject and someone who – partly at least – did their PhD on the subject, I can’t do that, I have to look a bit deeper into the whole concept of the margin for error and, perhaps, shed some light on why it comes about in the first place.

One thing that is glossed over (or perhaps even ignored) in the case law and by the profession generally is how variable valuation is – at least in regard commercial property valuation. Although we have come to understand that, for a ‘normal’ property in ‘normal’ market conditions, a variation in excess of +/- 10% can be viewed as being negligent, there is a lot of evidence that valuation is often a lot less ‘accurate’ than that. As an aside, I am surprised that this evidence has not been included in negligence claims.

There are two main ways of looking at the variability of valuations; seeing how accurately a valuation of a single property predicts a subsequent sale price of that property (after all, a valuation is meant to be a proxy for a sale under idealised assumptions) and, secondly, a measure of variance across a number of valuers valuing the same property.

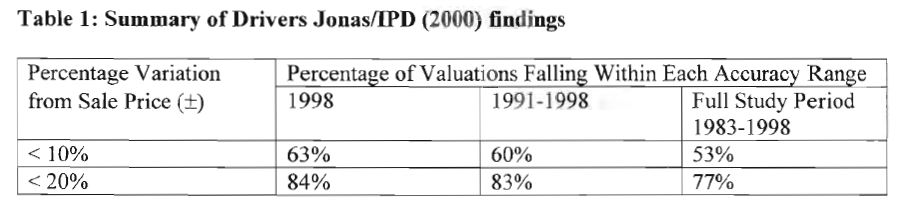

Turning to the first measure, the one looks at concrete sales of previously valued properties. This has been done for around 25 years by the IPD and Drivers Jonas. The first decade of their findings were quite startling for the profession:

Source: Boyd (2002) (http://www.prres.net/Papers/PRRPJ_No_2_2002_Boyd.pdf)

As can be seen, only just over half of all valuations over the period 1983-98 actually fell within the +/- 10% benchmark!

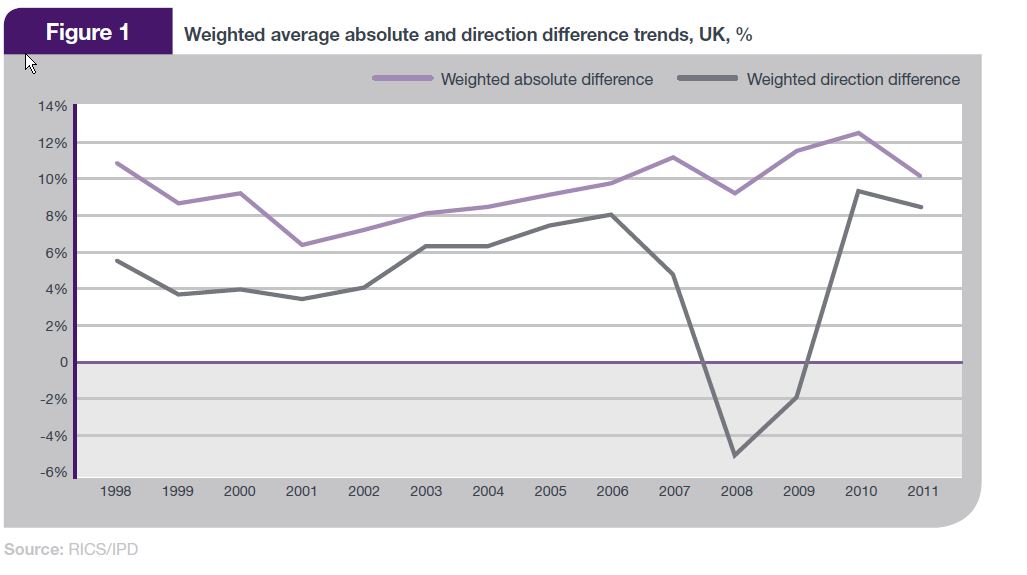

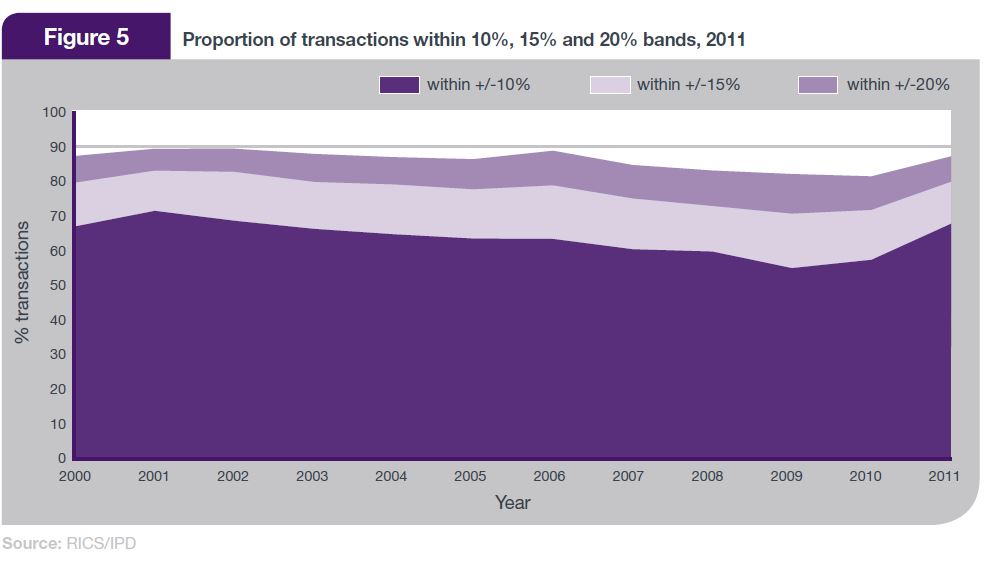

The study has been continued by the RICS in conjunction with the IPD – Have things improved? Well look at the figures below and draw your own conclusions:

Things have perhaps improved but there is no doubt that the mean variation is in excess of +/- 10% - this could be viewed as saying that the average valuation is negligent going by the court’s standard measure! This is silly of course – and there a lot of good reasons why sale prices often do not shadow a valuation (eg an investor may not sell unless they (a) are forced to or (b) receive a bid substantially above their own valuation) but I think you will be able to see my point that valuation is a lot less accurate than the profession actually thinks it is.

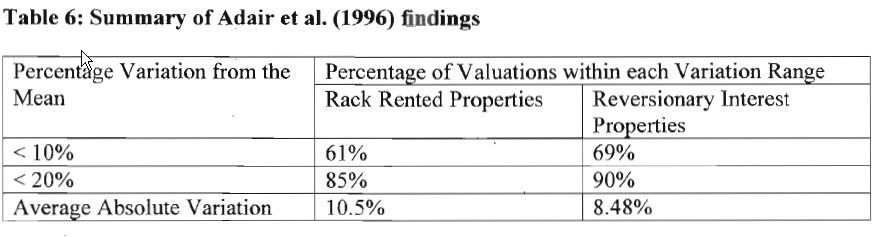

A better measure might be variance – the repeated valuation of the same property by a number of valuers independently. The problem with this is that this rarely occurs in practice – in fact one of the few times when it does is when a valuer is being sued for negligence and a number of expert valuations are carried out on the subject property – so this tends to be have to be examined under experimental/mock conditions.

A number of these studies have been done over the last 20 years, including some of my own, and the results have been pretty consistant. A representative study is the Adair et al one, a joint study by the universities of Ulster and Aberdeen, whose findings are shown in the table below:

Source: Boyd (2002) (http://www.prres.net/Papers/PRRPJ_No_2_2002_Boyd.pdf)

What does all of this add up to? Well firstly, it’s pretty clear that valuation is still an art and not a science, that for all the evidence that might exist to support it, a valuation is not a hard and fast figure. As valuers, we probably know all that, though, perhaps, we are probably not collectively aware of the extent of the variations in these opinions.

The second thing to be aware of is that, whilst the courts take a very narrow view of what is acceptable variance, the reality is rather irrelevant!

There is another stream of research, however, that might help valuers to avoid getting into a position where they might produce a valuation outside of these margins. This is the research into the process of valuation and the decision making involved – and this was the reason for the little exercise at the start which I will hopefully report the results of before the end of the day.

There is not sufficient time here to cover the topic in depth but there are two established factors that have been established over the last 70 years research into decision from a number of fields (including medicine and finance) that are very significant to producing a valuation: Anchoring and Adjustment and Confirmation Bias.

- Anchoring and adjustment heuristic is a mental shortcut that involves using a number or value as a starting point, and then adjusting one's answer away from this anchor; people often do not adjust their answer sufficiently. People who have to make judgements under uncertainty use this heuristic by starting with a certain reference point (anchor) and then adjust it insufficiently to reach a final conclusion.

- Confirmation bias is the tendency to favour evidence that supports existing perceptions.

Both of these are particularly critical in valuation. If you think about it, one of the first things that we look for when we start a valuation is to establish a starting point, a figure to place the property interest into the right place in the market place. If we were not able to do this we would waste a lot of time looking at evidence that was not particular relevant to us. Sometimes this process is an internal one; sometimes we get an external figure to anchor on such as a transaction or an asking price (and in case you have not guessed, this was what varied in the information I gave you). This is fine if the anchor is reasonably sound; if it is wrong then the evidence is that the adjustment from it tends to be insufficient.

This process is made worse by confirmation bias. If we have an opinion, humans seek out evidence that will tend to confirm this opinion whilst disregarding anything that contradicts it. This has been proved to happen time and time again in fields outside valuation – and, experimentally, several times with it.

I am not saying that this is the explanation for high variance in valuations and subsequent negligence cases but it does go a long way to understand just how valuers who do produce a valuation that is considerably out of step with the ‘true’ value of a property and why, against the evidence to the contrary, they do not adjust their figures.

A valuer having an awareness of behavioural traps in decision making will be one that is less likely to produce a negligent valuation.

Conclusions

The margin for error concept continues to be the main measure that the courts look to to establish whether a valuation is negligent.

In general:

- For ‘standard’ residential property, the margin of error required by a valuer could be as low as +/- 5%

- For a valuation of a one-off property, and most commercial properties, the margin of error will usually be +/- 10%

- If there are exceptional features of the property, or the market is thin or unstable, the margin of error could be +/- 15% or even higher.

This attitude of the courts is, however, out of step with the evidence from the wider market which shows that quite a high proportion of valuations have inherent variance in excess of 10% .

Research is being carried out into the sources of valuation variance/negligence, particularly in regards to behavioural issues. It is strongly suggested that valuers become more aware of the anchoring and adjustment heuristic and confirmation bias process that might lead them to not adjusting sufficiently from an unsound initial valuation opinion.

Dr Tim Harvard

235 Nantwich Road, Crewe, CW2 6NU,

01270 666 690